By Ramez Naam, Non-Executive Director and Investor at Distributed Energy

Solar is plunging in cost faster than anyone, including me, predicted. Today I’m publishing an update of my solar cost forecasts from 2015, with more data & improved methods. Solar is on path to become insanely, world-changingly cheap.

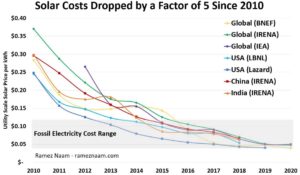

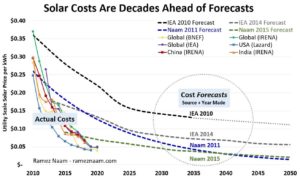

Over the last decade, from 2010 – 2020, the unsubsidized cost of solar electricity from utility scale projects has dropped by a factor of 5 or more. That’s consistent in global average data, and in the US, India, & China. Solar is now often competitive with new coal or gas.

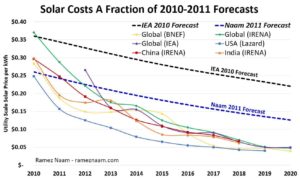

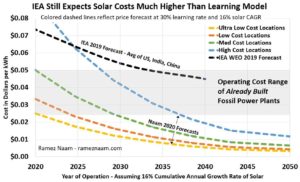

Solar has dropped in cost far faster than any forecaster expected. Solar prices in 2020 are half of what I projected in 2011. They’re a quarter of what the IEA projected in 2010.

Solar costs are now decades ahead of what most forecasts predicted. Solar prices are now:

- 7-10 years ahead of my 2015 forecast

- 10-15 years ahead of my 2011 forecast

- 30-40 years ahead of IEA’s 2014 forecast

- 50-100 years ahead of IEA’s 2010 forecast

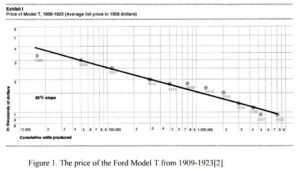

To model future solar costs, we’ll use the learning rate, also known as Wright’s Law. It predicts that every doubling of cumulative production of a technology leads to a consistent percent decline in cost. It applies as far back as the Ford Model T. More information on this can be found here.

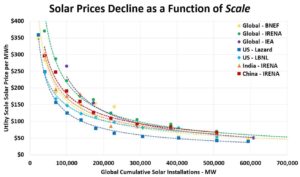

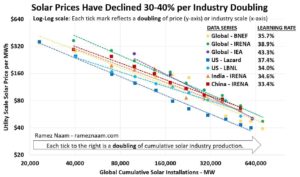

To see if Wright’s Law applies to solar, we need to look at the cost of solar electricity as a function how much solar the world has deployed (rather than solar cost over time). And we can see that solar costs have dropped smoothly as scale has increased.

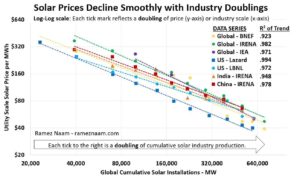

And this chart tells us that solar learning is fast. Incredibly fast. Solar electricity costs are dropping by an incredible 30-40% per doubling. That’s consistent across all 7 data series on this chart.

That’s an incredible, unexpectedly high learning rate. It’s roughly twice the learning rate found in most of the literature, in my 2015 forecast, and in reports from bodies like the IEA and EIA.

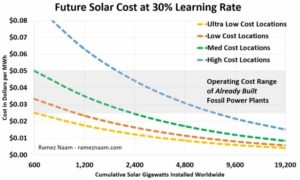

Let’s be conservative and use the low end of this range, a 30% learning rate. At 5 more doublings (32x current scale) the *average* cost of solar in sunny places would be 1 cent /kWh. Ultra-low cost deals would be half a cent. Even northern Europe would see 2 cents.

Astute readers will see that the far end of that scale is 20 TW of solar, or enough to supply roughly 2/3 of the world’s current electricity demand. That may seem utterly pathological. But there are many reasons to expect higher demand, and more use of the cheapest power.

Electricity demand is likely to rise over the coming decades, and demand for the cheapest electricity in particular, as:

1. A richer world. Incomes and consumption rise in the developing world.

2. Electric transport. Ground transportation becomes electrified, boosting global electricity demand by as much as 50%

3. Flexible demand. More and more electricity demand (including EV charging) becomes flexible, to use electricity at the hours that it’s cheapest (frequently meaning solar).

4. Cheap energy storage. Cheap energy storage allows shifting of solar (the cheapest electricity) to use in evening hours, increasing the amount of solar that can be productively used each day.

5. Industrial decarbonization. Cheap clean electricity is used to either power industrial processes or to power the creation of chemical energy carriers (e.g., hydrogen) that can be used for industrial processes such as making heat and cement, that are currently difficult to decarbonize.

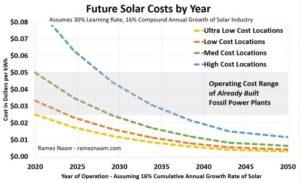

These future solar cost forecasts at a 30% learning rate also project costs far lower than the IEA’s most recent assumptions in their 2019 WEO. By 2030, a 30% learning rate projects solar costs 1/2 of IEA’s assumptions. By 2040, less than 1/4 of IEA’s assumptions.

Why have past forecasts been so wrong?

1. Academic studies often end at 2011, when less than 10% of today’s solar had been built.

2. IEA/EIA use much lower learning rates.

3. My 2015 forecast used US scale, instead of global scale, to find the learning rate.

Solar this cheap, if it arrives, will have a massive impact. It’ll help decarbonize electricity. It’ll also help decarbonize industrial processes that use direct heat today, either by electrifying them, or by creating cheaper green hydrogen. More in a future post.

At the same time, this forecast of cheap solar is NOT a panacea. 1. Learning could slow, or prices could hit a floor. 2. We need cheap storage for evenings. 3. We need cheap winter electricity in places like Europe, when days are short, & electricity demand is high.

In short, we need to continue to push for policies that help scale solar and fund additional innovation, and also continue to push for deployment & innovation in complementary energy sources like wind, geothermal, and nuclear.

All the same, this incredible pace of technological innovation – which was kickstarted by pro-solar policies in places like Germany – should give us a measure of hope. We have enormous innovative capabilities which we can bring to bear.

The full article can be found here. This is a republish, with permission from Ramez’s Twiiter.