By Ruchir Punjabi, Co-Founder, Distributed Energy

As I write this the stock market has just had its most recent downturn. The prophecy of the 10 year bull market continues, although the drops wipe out substantial value.

I had a small exposure in this market and was forced to heed to margin calls to hold my stock positions. Thankfully it was not a big exposure. This is my first bear market as an ‘investor’; when the last major crisis hit, I was still at University.

The idea of asset allocation is not new. Every investment advisor and smart investors will tell you to spread your risk on investments, to find the right balance for your risk profile. Thankfully, as a younger investor I understood that advice and already had a healthy mix of real estate, international stock, CFDs, bonds, commodities, cash and renewable energy.

I am writing this to tell you about why renewable energy, or more specifically solar assets are part of that investment mix.

Private equity funds and private wealth investors have been investing in renewable energy for close to a decade. The normal model is this: find a utility scale (very, very large) power buyer who is willing to buy power. Normally these are governments of different states or countries. Sign a ‘Power Purchase Agreement’ (PPA) for a period of 20 years or more and lock in rates from now. If the power buyer has a good credit rating and is not likely to default, find capital from large institutional investors and pay that capital upfront. Historically, utility scale renewable power plants have offered an IRR of 8%+ dollar returns across the world.

In the early stages the governments were willing to lock in “higher” rates (compared to conventional sources of power) to diversify their energy mix and invest in a greener future. However, over a period of time, as the deployment of renewable energy has accelerated, the cost of deploying these assets has reduced.

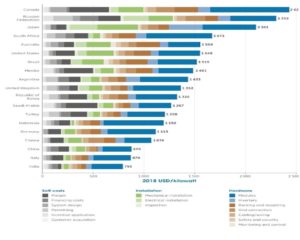

No energy asset has seen a higher drop in cost than solar panels in the last decade. At utility scale levels, this cost is as low as $500/kW in places such as India today. There are many estimates available online that show that this cost will continue to fall 10% every year for a while. The graph below is an extract from a study conducted by IRENA. It illustrates the margins involved in this business around the world in 2018 and how the cost of solar panel is a major component of the cost.

We have now reached a place where the per kW cost can actually make power a lot more affordable for energy consumers – especially businesses. In most countries including India and East Africa, governments subsidise residential electricity by charging businesses higher. This means businesses are usually paying more than 8c/kWHr. By having the cost of solar panel that’s already lower or, lowering, on an ongoing basis, we can position the same PPAs mentioned before and offer businesses a rate that is lower than their commercial grid rate.

In most of these businesses, electricity is a critical part of their business and if the right due diligence is done around their ability to generate cash and the stability of their business, we can actually install and supply power to them through solar that saves the business 20% or more on their bills while yielding 15%+ IRR annually over the length of the PPA. Further, if the asset or the asset pool is leveraged, the same IRR on the original equity amount shoots up past 20%.

As a type of asset, solar panels don’t move much. Their durability is fairly good long-term and with the right kind of preventative maintenance they should last 25 years or more. Given what electricity means to businesses who consume this power for their manufacturing, lights, compression moulding, cooling, etc – they usually pay their bills on time or their power gets cut. Also, these panels can be moved easily to different customers if the original customer defaults.

With such durability, and economics that work, solar power offers a unique advantage to an investor that is not dependent on market dynamics. If enough plants are aggregated, the risk of default can be minimized and the cash flow is highly dependable.

For portfolio allocation, an investor wants a good mix of assets ranging from high growth strategies, capital accumulation allocation, but also cash yielding and stable annuity assets. Of course, every investor has their preference around what matters to them. But in the end, there are few assets that offer the stability and annuity that solar assets do.

This is one of the main reasons why the likes of Warburg Pincus, Goldman Sachs and some of the largest investment houses in the world invest substantial funds into solar farms.

Distributed Energy is making access these kinds of new investments possible for smaller investors. Why should only the big investors get this opportunity. I for one, have already taken advantage of the opportunity, and invested part of my portfolio in solar based PPAs.