Renewable energy is a major driver for achieving sustainable life on earth, with promising potential in India – a country that ranks third in terms of its energy consumption, right behind China and the United States of America. It also ranks third in oil consumption with over 22 tonnes consumed annually.

With the ongoing depletion of oil and natural gas reserves and the cheaper cost of deploying renewable technology, now is a fantastic time to explore what this trend translates to in the renewable energy market in India this year. Renewable energy adoption in India considerably slowed down in 2020 but recovered by the end of 2021. The government played a pivotal role in catalysing the commissioning of auctioned utility-scale renewable energy projects. It also accelerated the distributed solar PV market with improvements in its renewable energy policies. Such government led implementations and alike have helped India to double its renewable energy capacity since 2020.

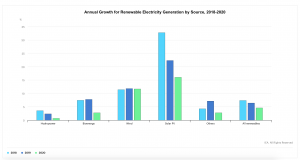

An Overview of India’s Renewable Energy Capacity

Many states in India have improved their renewable energy policies to invite more investment into the sector. North India for example, has a potential capacity of 363 GW, with various schemes being introduced to encourage early adoption of sustainable technology at a smaller scale.

The installed capacity of solar alone has increased by 18x, having gone up from 2.63 GW in 2014 to 49.3 GW in 2022.

As of May 2022, power production from renewable energy sources, with the exception of hydropower, stood at 19.31 billion units.

As of April 2022, India’s installed capacity peaked at 158.12 GW. This translates to about 39.43% of the total power capacity in India. There has been an additional 8.2 GW capacity addition in just the first quarter of 2022 when compared to the first half of 2021.

Renewable Market Developments

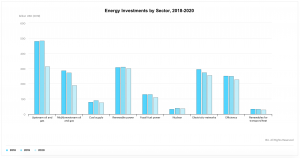

- Between April 2000 – March 2021, India has seen Foreign Direct investments (FDI) to the tune of USD 11.62 billion in the non-conventional energy sector. The data released by the Department for Promotion of Industry and Internal Trade (DPIIT) also shows an inflow of USD 70 billion, since 2014.

- According to British Business Energy, India is now ranked third in the world when it comes to attracting renewable energy investments.

Below are the market highlights that outline its potential.

- Renewable energy investment in India reached USD 14.5 billion in the first half of 2022, which is 125% more than the investment accrued in 2021.

- The Indira Gandhi International Airport (IGIA) in Delhi, became India’s first airport to be powered entirely on hydro and solar power. Solar installations meet about 6% of the airport’s energy demand.

- India was ranked globally third in the EY Renewable Energy Country Attractive index.

- Creduce Technologies – HCPL JV won the bid for India’s largest hydro power carbon credits project through its partnership with Satluj Jal Vidyut Nigam in February of 2022. This project will deliver over 80 million carbon credits.

- Husk Power Systems is a company working towards rural electrification. In February 2022, this firm secured a USD 42 Million loan from the Indian Renewable Energy Development Agency (IREDA). This funding would go towards developing off-grid power sources with renewable techology in hard to access rural communities in India.

- Karnataka will see investments worth an estimated USD 1.53 billion into renewable energy projects. The projects will be executed by Ayana Renewable Power Pvt Ltd.

- India’s largest energy service provider, Tata Power was awarded a contract by the Maharashtra State Electricity Distribution Company Limited. The project grants end-to-end execution rights to Tata Power Solar, a subsidiary of Tata Power. The 300 MW wind-solar hybrid power plant will be spread out over 130 acres in the Satara District.

- Reliance New Energy Solar Limited made two new acquisitions in October, 2021. The two firms were Sterling & Wilson Solar, based in India, and REC Solar Holdings, a Norwegian firm. The acquisitions exceeded USD 1 billion, and are key to achieving the promised 100 GW of solar power proposed by RNES Limited in Jamnagar.

- Similarly, Adani Green Energy acquired SB Energy India in October, 2021 for USD3.5 billion to venture into India’s renewable energy sector.

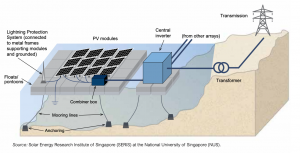

- The NTPC is commissioning India’s largest floating solar power plant in Ramagundam, Telangana, with an installed capacity of 447 MW.

- The Solar Energy Corporation of India (SECI) is implementing large-scale central auctions for solar projects. It has already awarded contracts for 47 parks that will have a combined capacity of 25 GW.

Government Policy Updates to Facilitate the Renewable Market Growth in India

- A budget of USD 132 billion was allocated for SECI, the governing body responsible for the development of India’s entire renewable energy sector.

- The Union budget also allocated USD2.57 billion to a PLI scheme that pushed for the manufacturing of high-efficiency solar modules.

- Nepal and India agreed to form a joint Hydro Development Committee in February, 2022.

- Prime Minister Narendra Modi proposed to increase India’s renewable energy capacity to 500 GW to meet 50% of India’s energy demand at the COP-26 Summit in Glasgow.

- The Ministry of Power announced an addendum that would reduce the financial stress of stakeholders and ensure timely cost recovery in power production.

- The latest rules for the purchase and consumption of green energy encourages large-scale energy consumers like industries to explore renewable energy for regular operations.

- The Rooftop Solar Programme Phase II rolled out by the Ministry of New and Renewable Energy will oversee the adoption of rooftop solar in urban and rural areas. It aims to reach a capacity of 4000 MW in the residential sector, accelerated by subsidies.

- NTPC Renewable Energy Ltd, is set to build a 4750 MW renewable energy park in Rann of Kutch in Gujarat. This will become India’s largest solar park.

- The Government is also investing USD 238 million as part of a national mission to research and implement advanced ultra-critical technologies for cleaner fossil fuel consumption.

- The Indian Railways is implementing energy efficiency measures and maximizing clean fuel usage. This undertaking is expected to cut down emission levels by 33% by 2030.

All of the above schemes and revisions will ease FDI in India’s renewable energy market. It also provides a strong business case to go solar, for both business owners and investors alike. Distributed Energy is an experienced platform aggregator that enables renewable energy projects in underserved economies. The team leverages its technical expertise in optimizing clean energy production. With projects spread across Asia and Africa, businesses and investors can choose to help inch the planet towards net-zero. Visit www.de.energy to learn more about Distributed Energy and what it is like to invest in solar.

The European Union (EU) has already drawn up a comprehensive strategy on sustainable finance through the European Banking Authority (EBA).

The European Union (EU) has already drawn up a comprehensive strategy on sustainable finance through the European Banking Authority (EBA).

In the most recent

In the most recent